Kelly % = W – [(1 – W) / R]

W = Probability of Profit

R = Win/Loss

The Kelly Criterion illustrates this concept very well. It shows you what ones risk as a % of their capital should be. For example, if a trader has a W of .85 and a .5 R (.5/1) then they have a Kelly Criterion of .55 or 55% of their capital can be used to make this trade. However, lets say they have a W .6 and an R of .5 (.5/1) they will have a Kelly of -.2 or -20% of your capital. This is because there is no edge in the long run considering this certain trade. I could run several tests and find this almost never works; therefore, the returns are sharply negative. Options sellers need to keep this in mind because it means letting your losses run is not an acceptable strategy, and since your risk is greater than your reward on a single trade the optimal loss point is something that need to be considered.

However, the premuim buyer also needs to keep the Kelly Criterion in mind . If they are long an option with a .25 W and a 3 (.75/.25) R then that trader can only break even (Kelly Criterion is 0), and after commisions and slippage they would be a small loser. The premuim buyer has to have an understanding of their probability of profit compared to their risk reward because the trader might make money over 10 or even 100 trades, but over 10,000 trades it is extremley unlikley.

If one want to trade like a Casino or the house one has to have a very good understanding of edge compared to ones sizing. If we assume returns are distributed randomly even with a large edge returns can be very volatile. Sizing is key because the bigger the edge the larger the optimal position size is; the smaller the edge optimal postion size also becomes smaller, but considering returns are randomly distributed the trader needs to have many occurences, but always have edge working in ones favor. If the trader has proper sizing the volatility in returns is much less because little trades can work for the trader overtime while trades with much larger edge can provide the meat of ones returns while the small trades are paying little bit of money every month or every year.

The reason this concept is so important is even with edge a trader can have periods of time where they peform poorly. This is due to the random element in distribution of returns. This does not mean the markets are a "random walk", but it does mean we can not predict the future, and we can only play the numbers we see now.

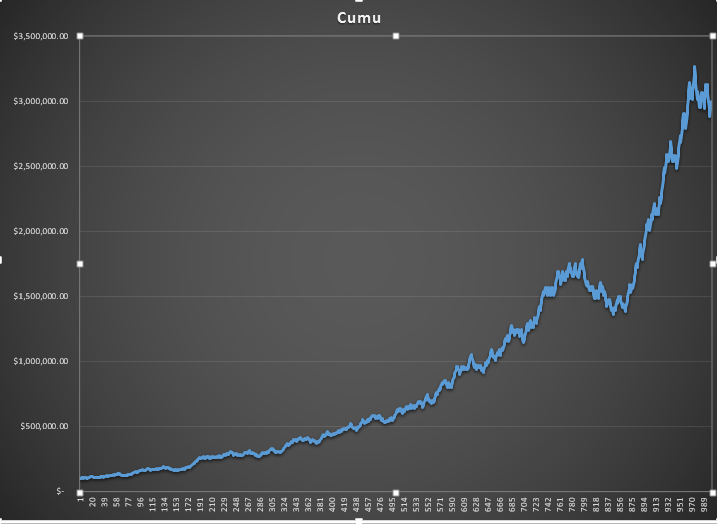

For example, the chart below illustrates a simulation of an options trade with a 55% probability of sucsess and a reward to risk of 1 and 2% of the portfolio is used. As shown, the returns over 1000 occurences is muted. There is a low chance of this with this edge, but there are times when your "edge" does not work.

In the chart below, I am using the same 55% probability of profit and a Reward/Risk ratio of 1. The returns are ridicoulously huge for such a low risk strategy; this also is unlikley.

However, As we get to several different tests the results are closer to each other.

The data seems to illustrate the returns reaped from trading like a casino does business o. However, the casino understands size well also. That is why they put table limits in place, and this is why us traders need to always need to stick to our risk guidlines. There can be wild girations in returns even over 1000 occurences or more. The biggest mistake many traders make besides improper size is changing strategies when something doesn't work. If you have found positive EV in a certain strategy stick to it because you can have large volatility in returns during certain periods of time, but over many years and occurences you are going to find yourself with a large positive return. This, for example, is why buy and hold works or selling index premuim works so well. They both have edge, and it is only a matter of the risk you are willing to take and proper sizing.